For international investors, the contrast between China’s growth process and the rest of the world could not be greater than it is today. As most other major economies aim to raise interest rates and stop stimulus measures to curb inflation, the massive economic stimulus based on the construction sector, which Beijing had been trying to avoid for the past two years, is suddenly back in the news.

Par Claire Xiao, Credit Specialist, Lucette Yvernault, Head of Systematic Income, Chuin Wei Yap, Investment Secretary

Chinese politicians face old problems in new economic recession. There are growing indications that the world’s second largest economy needs to increase, but without reviving the borrowing frenzy.

Faced with a gradual rise in interest rates, China’s central bank has lowered interest rates since July 2021, in an effort to free up liquidity in the country’s banking system. Last series of relaxation measures was decided at the end of January and we believe that a further interest rate cut is likely.

For international investors, the contrast between China’s growth process and the rest of the world could not be greater than it is today. Most major economies, including the United States and Europe, are preparing to raise interest rates and discontinue stimulus measures to curb inflation in stages. In China, where inflation is still low, monetary policy has eased and a massive economic stimulus based on the construction sector, which Beijing had tried to avoid for the past two years, is suddenly back on the agenda.

Intervene early enough?

When it comes to policy-making, the risk of mistakes is high in all areas. In the United States, there is a constant debate about whether the US Federal Reserve is doing too little and too late to keep inflation in check.

In China, Beijing is tackling the same problem, but in the opposite direction: doubts persist about the authorities’ ability to intervene quickly and effectively enough to revive the main growth pits – especially in the real estate sector, which, with construction and related industries, represents more than a third of economic output. On the other hand, the opening of credit port floodgates in the past has weighed on the economy with persistent industrial overcapacity, bad debts and other systemic imbalances that could further disrupt the financial system in the long run.

Examined in detail, the timing of recent government action is indicative of how it is trying to seize the initiative without going overboard. Although this was generally expected, the interest rate cuts came in mid-January earlier than expected. The Central Bank, best known for its measured relations, said the day after it was intervening to prevent a “credit crunch”. The harsh tone seemed intended to boost confidence in Beijing’s ability to cope with the economic collapse.

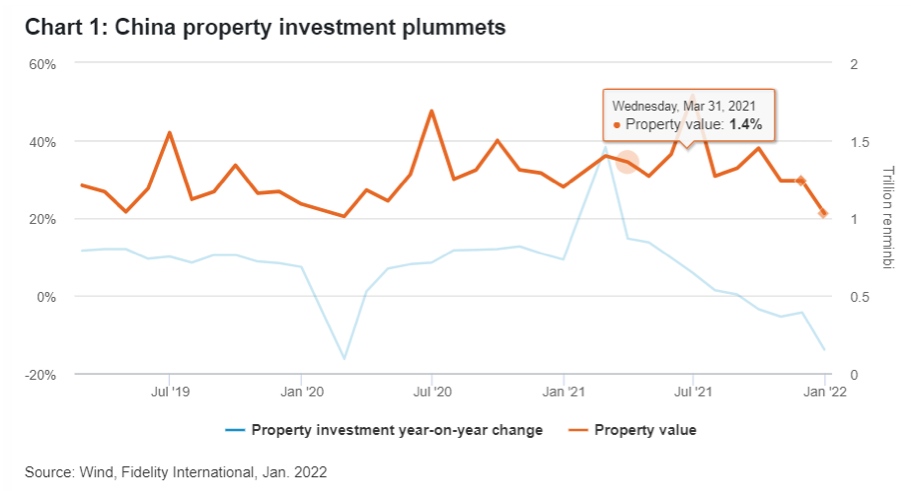

Recession in the real estate sector

As slower real estate and land sales slow to growth by the end of 2021, Chinese banks were given quantitative lending controls (“window guidelines”) to expedite mortgage approvals, and advice to apply. Realtors, however, are still as sluggish, suggesting a deeper problem in deteriorating demand. A recent Chinese policy, which has imposed restrictions on apartment ownership, for example, may have gone too far and stifled buyers’ appetites. The development of municipal bonds, of the kind that finances the development of infrastructure, has slowed down considerably.

Policymakers are now considering broader measures aimed, among other things, at making it easier for real estate producers to access their pre-sale funds, which were previously frozen in custody accounts. To be effective, some of these measures require very close coordination between the state, municipalities and municipalities. In our opinion, if such changes in the regulatory framework are unsatisfactory, further interest rate cuts should take place in the first half of the year. That being said, the downturn in real estate is not the whole story: there are pockets of resilience in the Chinese economy, including in exports, manufacturing, services, to name a few.

Fidelity offers financial services that involve the purchase and / or disposal of financial instruments within the meaning of the Federal Financial Services Act (LSF). Fidelity does not need to verify the appropriate and adequate financial services it provides under FinSA. All investments must be made on the basis of the current prospectus and the FIB (Basic Information Sheet), which is available free of charge, together with the Articles of Association and the latest annual and half-yearly reports of our distributor, from our center. de Service Européen in Luxembourg, FIL (Luxembourg) SA, 2a rue Albert Borschette BP 2174 L-1021 Luxembourg, or from our Swiss representative and payment service, BNP Paribas Securities Services, Paris, Zurich branch, Selnaustrasse 16, 8002 Zurich. This promotional material is published by FIL Investment Switzerland AG. The information in this promotional material should not be construed as an offer or offer to make an offer to acquire or dispose of the financial products mentioned in this promotional material.

Start investing your money in cryptocurrencies and get Free Bitcoin when you buy or sell 100$ or more if you register in Coinbase